[ad_1]

Wall Street analysts’ price targets are not guaranteed, but they can be a good starting point for finding promising investments. One stock that has caught my attention recently is an e-commerce focused pet retailer. chewy (NYSE:Chewy).

The company’s stock price is currently around $16 per share, but Wall Street analysts are fairly optimistic about the stock, maintaining an average price target of $31.62. This means a 97% upside potential. The company recently received an updated Buy rating from analyst Eric Sheridan. goldman sachs and trevor young barclaysset price targets at $36 and $30, respectively.

After reviewing Chewy’s recent performance and the strategy outlined by management at its December investor day, I can’t help but agree with Wall Street. Down 86% from its all-time high, Chewy looks like an outstanding growth stock to buy at its current all-time low valuation.

America’s No. 1 pet specialty retailer

Despite only being founded in 2011, Chewy has grown to account for about one-third of the online pet retail market and generated more than $11 billion in sales in the past year. Since its initial public offering (IPO) in 2019, Chewy’s business has been strong, with revenue tripling and its active customer base nearly doubling to 20.3 million.

However, the company’s sales growth slowed to just 8% in the most recent quarter after a 50% increase in sales in 2021 due to the pandemic-driven sales surge. This dramatic slowdown explains the deterioration in market attitudes towards the stock, but there are still plenty of reasons to be excited about the business’ growth potential.

First, Chewy operates in the incredibly resilient $144 billion pet retail industry, which is expected to grow 6% annually through 2027. Earnings growth has been declining recently, but it should start to stabilize.

To quantify the company’s sales stability, consider that 85% of its revenue comes from non-discretionary consumables and healthcare products. These necessary (and typically recurring) sales help explain why Chewy generates a whopping 76% of its revenue from customers who use its subscription service, Autoship. . Autoship, which grew 13% in the third quarter, continues to outpace Chewy’s overall revenue growth and provides sticky and steady sales.

Second, Chewy’s healthcare division continues to do well, with sales increasing from $1 billion in 2018 to $3 billion last year and now representing nearly 30% of total sales. This division consists of pet medicine, insurance, PetMD, telemedicine, and veterinary management systems and aims to help the company become a one-stop shop for veterinarians. anything Pet related. These healthcare businesses are critical because they attract high-value customers who go above and beyond for their furry friends while achieving profit margins that are 10 percent higher than the retail division.

To top things off, Chewy continues to expand its private label and advertising sales, adding two more high-margin units. Currently, these private label brands account for about 5% of sales, but are expected to grow to 15% of the company’s revenue in the long term. Private label products have a 7 percentage point higher profit margin than national brands, and have the potential to further boost Chewy’s profits.

Similarly, the company launched sponsored advertising options less than a year ago. Management believes this will result in gross margins of around 70%, further boosting profits.

Margins continue to improve despite spending in growth areas

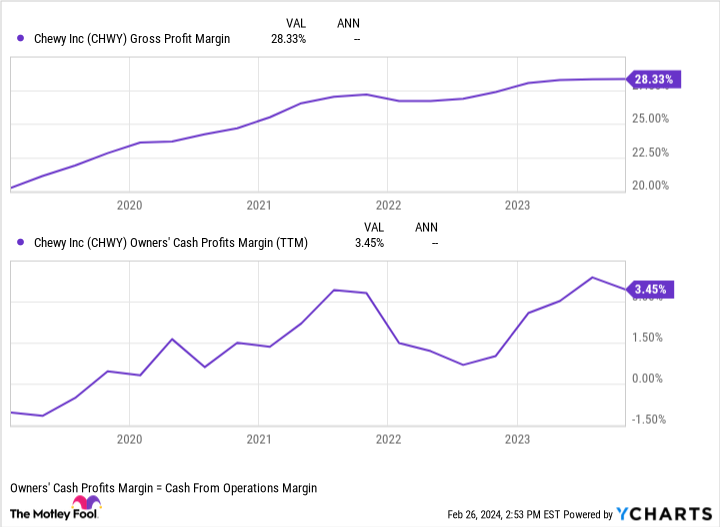

Perhaps the most important part of the bullish investment thesis for Chewy is its improved margins. The company is rationalizing its operations while testing new growth ideas, driven by the high-margin growth areas mentioned above, such as health care, private labels, and advertising sales.

Gross profit margin data by CHWY Y chart.

Steadily increasing gross margins as logistics inched closer to peak efficiency, Chewy steered the company toward consistently generating positive operating cash flow (CFO). Even accounting for stock-based compensation, Chewy’s CFO has maintained positive performance over the past two years, allowing the company to fund its growth goals internally.

Lowest valuation ever

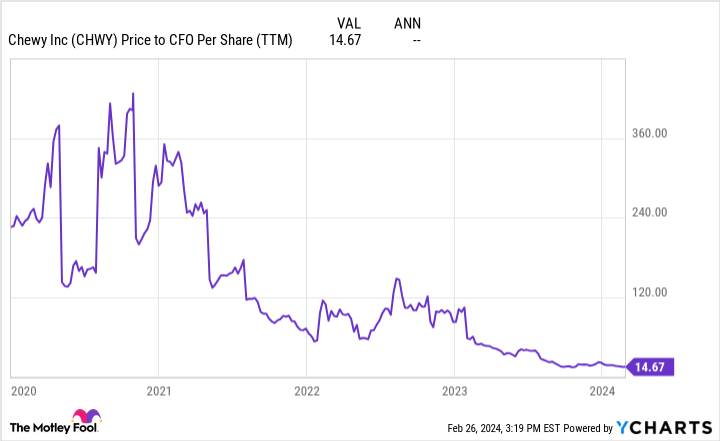

Most importantly for investors, despite Chewy’s exceptional non-discretionary sales, promising growth options and improving margins, the company’s price-to-CFO (P/CFO) ratio is at an all-time low. is.

This small P/CFO ratio looks attractive considering its large e-commerce peers. Amazon, which retains a ratio of 22 despite being much more mature. Even better, Chewy is just emerging from a hyper-growth phase and is far from being optimized for maximum cash generation. The company’s P/CFO multiple of 15 looks even cheaper, as management expects the 3.5% CFO margin to roughly double over the long term as Chewy’s operations improve.

All these factors, not to mention the company’s No. 1 ranking in Forrester’s Customer Satisfaction Index, make Chewy a great choice to add to your portfolio at such a discount and keep for decades. looks like a great investment.

Should you invest $1,000 in Chewy right now?

Before buying Chewy stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks Investors can buy now…and Chewy wasn’t one of them. These 10 stocks have the potential to generate impressive returns over the next few years.

stock advisor provides investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks each month.of stock advisor Since 2002, the service has more than tripled S&P 500 returns*.

See 10 stocks

*Stock Advisor will return as of February 26, 2024

John Mackey, former CEO of Amazon subsidiary Whole Foods Market, is a member of the Motley Fool’s board of directors. Josh Kohn-Lindquist has no position in any stocks mentioned. The Motley Fool has positions in and recommends Amazon, Chewy, and Goldman Sachs Group. The Motley Fool recommends his Barclays Plc. The Motley Fool has a disclosure policy.

1 Growth stocks are trading at record low valuations, could rise 97%, according to Wall Street The article was published by The Motley Fool

[ad_2]

Source link