before its dividend goes ex-dividend.")

[ad_1]

Regular readers know that we love Simply Wall Street Dividends. Broadridge Financial Solutions, Inc. (NYSE:BR) is set to trade ex-dividend in the next four days. The ex-dividend date is typically set one business day before the record date. The record date is the deadline by which you must be listed on the company’s books as a shareholder in order to receive dividends. The ex-dividend date is an important date to be aware of, as purchasing stocks after this date may result in delayed settlements that will not show up on the record date. Therefore, if you purchased Broadridge Financial Solutions shares after March 14th, he will not be eligible to receive the April 5th dividend payment.

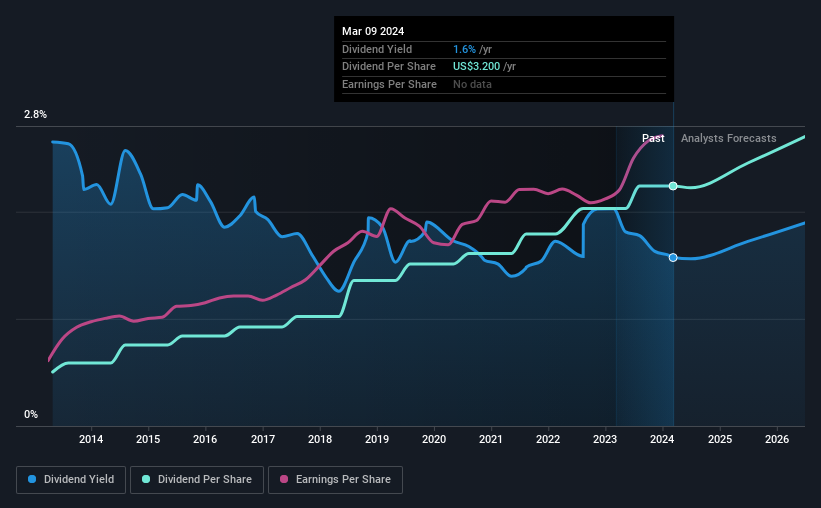

The company’s next dividend will be US$0.80 per share. Last year, the company distributed a total of US$3.20 to shareholders. Last year’s total dividends show that Broadridge Financial Solutions has a yield to maturity of 1.6% on the current stock price of $203.55. Dividends can be a significant contributor to investment returns for long-term holders, but only if they continue to be paid. So we need to investigate whether Broadridge Financial Solutions can afford its dividend, and if the dividend could grow.

See our latest analysis for Broadridge Financial Solutions.

If a company pays out more in dividends than it earned in profit, then the dividend might become unsustainable – hardly an ideal situation. Broadridge Financial Solutions paid out 53% of its profits to investors last year, which is a normal payout level for most companies. A useful secondary check is to evaluate whether Broadridge Financial Solutions generated enough free cash flow to pay its dividend. Fortunately, the company paid out just 37% of its free cash flow over the past year.

It’s positive to see that Broadridge Financial Solutions’ dividend is covered by both profit and cash flow. This usually indicates that the dividend is sustainable, as a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company’s payout ratio and analyst estimates of its future dividends.

Are profits and dividends growing?

Stocks in companies that generate sustainable earnings growth often offer the best dividend prospects, since it’s easier to lift dividends when earnings are rising. Investors love dividends, so if earnings fall and the dividend is cut, you can expect the stock to sell off heavily at the same time. That’s why we’re relieved to see Broadridge Financial Solutions’ earnings per share have grown at 9.6% per year over the past five years. Although earnings have been growing at a reliable rate, the company is distributing a large portion of its earnings to shareholders. Therefore, it is unlikely that the company will be able to reinvest significantly in its business, which could portend slower growth in the future.

Another important way to measure a company’s dividend prospects is by measuring its historical dividend growth rate. Over the past 10 years, Broadridge Financial Solutions has grown its dividend at an average annual rate of about 16%. We’re pleased to see that dividends have grown along with profits over the years, and this could be a sign that the company intends to share its growth with shareholders.

conclusion

Does Broadridge Financial Solutions have what it needs to maintain its dividend payments? With earnings per share growing slowly, Broadridge Financial Solutions is generating more than half of its profits and free cash flow. Although less than half of the dividend was paid out, both payout ratios are within the normal range. In summary, Broadridge Financial Solutions looks okay on this analysis, but it doesn’t appear to have any outstanding opportunities.

In that regard, you should investigate what risks Broadridge Financial Solutions faces.Every company has risks, and we found that 1 warning sign for Broadridge Financial Solutions. you should know about.

If you’re in the market looking for high dividends, we recommend: Check out our selection of high-dividend stocks.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and the articles are not intended as financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link