[ad_1]

March 8th was a rough day for the stock market.shares of Nvidia (NASDAQ:NVDA) It soared to an all-time high of $974, but fell more than 10% from that high to end the day at $875.28.At its peak, he was less than 9% away from being surpassed by Nvidia. apple (NASDAQ:AAPL) In terms of market capitalization. When I got closer, it was just over 20% of the distance.

Considering Nvidia’s big swings, it seems very likely that this stock will outperform Apple and become the next most valuable “Magnificent Seven” stock. microsoft. Here’s why Nvidia can continue to outperform Apple in the short term, but why Apple is a better buy in the long term.

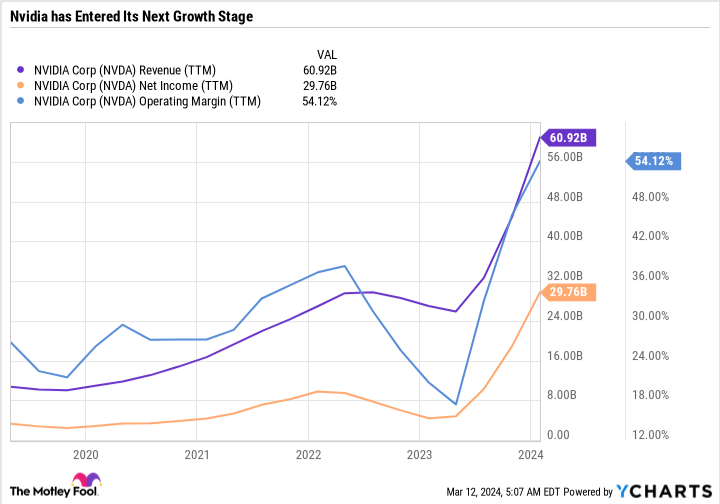

Revenue drives Nvidia’s story

Nvidia isn’t an unprofitable growth stock rising solely on optimism and greed (although those are factors). The business is doing phenomenally well, achieving levels of sales and profit growth along with margin expansion.

The only concern with Nvidia is its valuation. The price-to-earnings ratio (P/E) based on trailing 12-month (TTM) earnings is 73.6. However, the consensus analyst forecast is for Nvidia’s earnings per share (EPS) to more than double from $11.90 in fiscal 2024 to $24.50 in fiscal 2025. This gives Nvidia a forward P/E of 35.7, which is much more reasonable.

The easiest way for Nvidia to overtake Apple in market capitalization is for investors to keep bidding up the stock. But the more realistic question is whether Nvidia’s earnings can meet expectations.

Nvidia is scheduled to report full-year 2025 results in late February or early March next year. If the company reports earnings of $24.50, the stock price would likely rise even higher, especially if there is optimism about further growth going forward. A company leading the artificial intelligence (AI) revolution that has more than doubled its revenue with high profit margins probably deserves a premium valuation of around 2x. S&P500.

Nvidia has the highest P/E of the Magnificent Seven companies, but the company is approaching the point where it’s rising too fast.

Nvidia benefited from increased revenue and an expanded valuation. While it’s hard to assume valuations will continue to expand, the stock could still rise if the first half of 2025 goes as analysts expect. Expecting higher earnings in each new quarter will push the trailing-12-month numbers higher and lower the P/E ratio, leaving room for the stock to rise to fill the gap. There’s nothing better than earnings growth in the stock market, but at the moment Nvidia has it, Apple doesn’t.

Acquiring Apple when it was unpopular was historically a genius move.

So if Nvidia can move forward so easily, why is it better to buy Apple? Simply put, I think this setup is a better investment for Apple. Nvidia may be a better deal, but a more reliable way to build wealth is through long-term compounding investing.

Market sentiment is negative towards Apple. So negative, in fact, that Apple is trading at a discount to his S&P 500. The only reason this would happen is if something major went wrong with Apple. The company has its challenges, but none of them justify the decline in performance we’ve seen over the past six months.

The summary of why Apple stock is under pressure is that major AI monetization announcements (from Nvidia, Microsoft, and others) are not gaining traction. meta platform have). iPhone sales are declining in China, and overall growth is slowing. But Apple has endured times like these before, and has survived the competition.

piper sandler‘s Fall 2023 survey found that 87% of Gen Z own an iPhone, 88% expect their next phone to be an iPhone, and 34% own an Apple Watch. The iPhone is essentially a consumer staple in the United States, and it’s also growing well in international markets outside of China.

Investors should focus more on Apple’s ability to further monetize existing devices through services and AI than its competitors. The key for Apple has always been to increase the depth (services) and breadth (more products like phones, computers, tablets, wearables, earbuds, etc.) of its ecosystem. Continued spending growth for lifelong customers depends on product improvements.

Apple is under pressure to make a big contribution this summer to drive iPhone demand and upgrades. If Apple makes improvements that spur growth, the stock could soar. But even if they don’t, they can generate significant amounts of additional cash to make acquisitions and grow that way, or to return cash to shareholders while maintaining a strong balance sheet.

Apple’s brand, market position, and financial health give it the time and space it needs to make mistakes. The company is known for not attracting investors and only makes announcements when it believes a product or service is ready.

Apple has a better risk/reward profile than Nvidia

For Nvidia to continue to grow, it will need to meet very high revenue projections. The semiconductor industry is also highly cyclical, and a decline in customer spending could stall its growth trajectory. Nvidia may continue to grow at a breakneck pace in the short term, but it will eventually slow down. When that time comes, investors may be reluctant to give Nvidia a multiple of 3x the market average.

Apple, on the other hand, is already well-valued and has a clear path to regaining Wall Street’s support.

I don’t have a crystal ball, but if I had to guess, I’d say Nvidia will be worth more than Apple at some point. But he thinks that 3-5 years from now, Apple will be worth more than his Nvidia and will be a safer, less volatile investment.

Nvidia stands out as a high risk/high potential reward investment, while Apple is more of a low risk/medium potential reward investment. Investors who are confident that high demand for Nvidia’s products will continue will want to look at the quarterly earnings report to understand how important earnings play in the story. Nvidia has already seen strong returns, and investors should expect more reasonable returns going forward.

Should you invest $1,000 in Nvidia right now?

Before buying Nvidia stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks What investors can buy right now…and Nvidia wasn’t among them. These 10 stocks have the potential to generate impressive returns over the next few years.

stock advisor We provide investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks every month.of stock advisor Since 2002, the service has more than tripled S&P 500 returns*.

See 10 stocks

*Stock Advisor returns as of March 11, 2024

Randi Zuckerberg is a former head of market development and spokesperson at Facebook, sister of Meta Platforms CEO Mark Zuckerberg, and a member of the Motley Fool’s board of directors. Daniel Felber has no position in any stocks mentioned. The Motley Fool has positions in and recommends Apple, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: His long January 2026 $395 call on Microsoft and his short January 2026 $405 call on Microsoft. The Motley Fool has a disclosure policy.

Can Nvidia rise 21% and become the second most valuable ‘Magnificent Seven’ stock, surpassing Apple?Originally published by The Motley Fool

[ad_2]

Source link