[ad_1]

(Bloomberg) — Federal Reserve policymakers may finally be on the brink of cutting interest rates.

Most Read Articles on Bloomberg

Ahead of this week’s two-day policy meeting, which concludes in Washington on Wednesday afternoon, investors are placing near-even odds on the prospect that the U.S. central bank will start lowering borrowing costs in its next decision in March. .

That’s why Fed Chairman Jerome Powell’s press conference, and every signal he sends or not, will be very important. It all depends on how Mr. Powell and his colleagues have read the recent flurry of economic data.

Meanwhile, inflation numbers continue to surprise on the downside. The Fed’s priority indicator slowed to 2.9% in December, falling below 3% for the first time since early 2021, according to data released Friday.

On the other hand, personal consumption continues to be surprisingly strong. There is no doubt that the downdraft of inflation is pushing up prices, but some may still be concerned that upward pressure on prices will rise again.

Bloomberg Economics says:

“The Fed is poised to take steps to lower rates in the coming months. We expect the Fed to begin lowering its target range for the federal funds rate in March, aiming for a soft landing.”

-Stuart Paul and Estelle Wu.

Fed decisions aside, more U.S. data will be available next week. The most important will be Friday’s monthly employment report. Tuesday’s job numbers and consumer confidence data, as well as the release of the quarterly employment cost index during Wednesday’s Fed meeting, will also help gauge how strong the spending outlook actually is.

Looking north, Statistics Canada releases gross domestic product data by industry for November after three consecutive months of flat growth. Without the massive population surge caused by uncontrolled temporary migration, the economy would have shrunk.

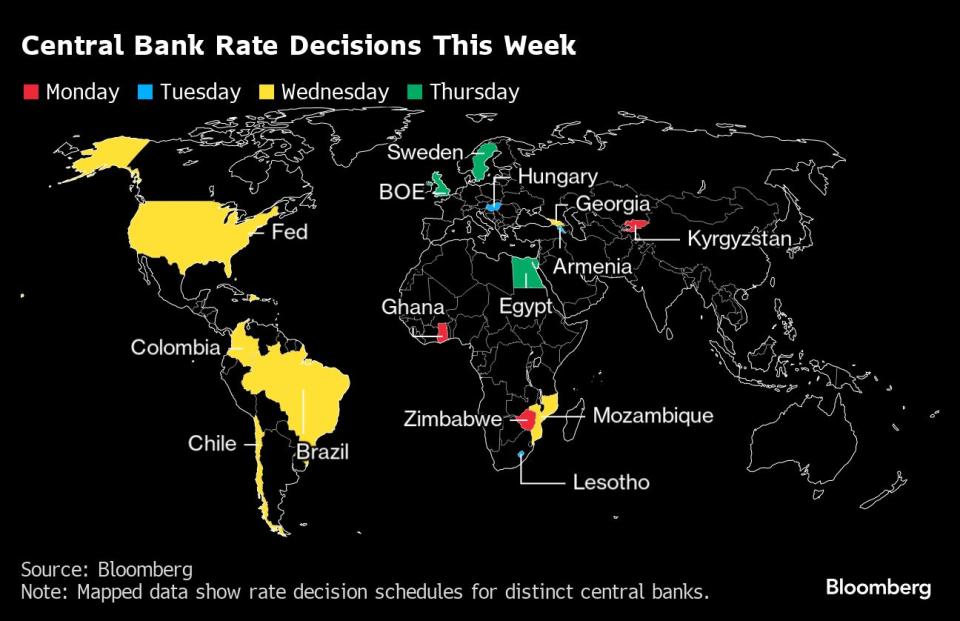

Elsewhere, decisions by the British and Swedish central banks could leave interest rates on hold while three central banks in Latin America cut rates.

Investors are also keeping an eye on euro zone inflation, GDP data and Chinese business research, with the International Monetary Fund releasing new forecasts on Tuesday.

Asia

China will release a Purchasing Managers Index on Wednesday that sheds light on the current state of the world’s second-largest economy.

Both manufacturing and services have slumped since September, further deepening the decline in factory activity as debate continues over the need for further stimulus to support sputtering growth.

The official figures will be followed by China’s private sector PMI report and corresponding figures for other countries in the region, where activity levels have slumped, partly due to the lack of a zipper in its giant neighbor.

This week begins with the Monetary Authority of Singapore switching to quarterly meetings, the first decision since long-time director-general Ravi Menon stepped down.

A summary of Bank of Japan board members’ opinions at their January meeting may provide further clues as to how close the bank is to raising interest rates for the first time since 2007. March or April is expected to be a very live meeting.

The Philippines, Taiwan and Hong Kong will release their fourth quarter economic growth results later this week.

Australia’s quarterly inflation figures are due to be released on Wednesday, with the economy expected to cool further just days before the central bank decides on policy at its first meeting of the year.

South Korea’s trade and inflation statistics, which provide insight into global trade trends, conclude this week.

Europe, Middle East, Africa

In Europe, three central bank decisions will attract attention.

-

The Bank of England may back away from threatening to raise interest rates again if necessary, after UK wage growth slowed to its fastest pace on record. But there are reasons to be cautious, especially after data showed an unexpected acceleration in inflation last month. It’s Thursday.

-

Riksbank officials have already said they see no need to raise borrowing costs again, but today’s decision could signal a determination to keep interest rates high for the time being.

-

In Hungary, policymakers could cut borrowing costs further on Tuesday. Most economists expect a 100 basis point (bp) cut to 9.75%.

This week is also important for data, with European Union member states set to release figures for both growth and inflation.

Belgium and Sweden released such reports on Monday, followed by several other countries the following day, including Germany, France, Italy and Spain.

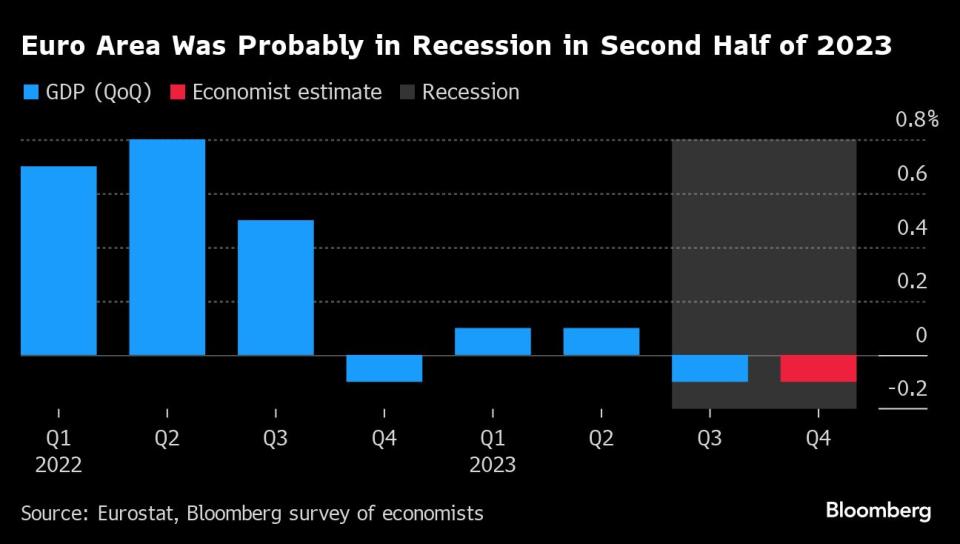

For the eurozone, economists expect the result to be a 0.1% contraction in the second quarter, which would meet the standard definition of a recession.

Inflation reports from across the region are also expected, culminating in results from across the currency bloc on Thursday.

That figure is expected to be 2.7%, still significantly above the European Central Bank’s target, but the so-called core gauge, which strips out energy and such volatile factors, is likely to remain even higher.

Outside of Europe, several other central banks are also expected to make announcements.

-

The Bank of Ghana’s decision on Monday puts the possibility of a rate cut in jeopardy. Inflation continues to slow and real interest rates are among the highest in the world. Still, the IMF has warned against easing.

-

On the same day, Zimbabwe is likely to outline plans to deal with the collapse in its currency, which has fallen by more than a third against the dollar on official markets since the start of the year.

-

Lesotho, which pegs its currency to the South African rand, may follow its neighbors on Tuesday and keep its key interest rate at 7.75% to support the economy.

-

Mozambique is likely to keep borrowing costs unchanged to curb inflation, even after the IMF said on Wednesday there was room for cuts.

-

Egyptian officials are scheduled to meet the next day amid the worst economic crisis in decades, with investors expecting an eventual currency devaluation. Discussions with the IMF continue, but the central bank is likely to keep the policy rate at 19.25%.

Among data highlights, Wednesday’s data could show Saudi Arabia’s economy contracted for the second straight quarter at the end of 2023, after a contraction that largely reflected oil production cuts to boost prices. . This has gone from one of the fastest growing members of the Group of 20 to one of the laggards.

latin america

Brazil’s central bank on Wednesday cut interest rates by half a percentage point for the fifth time in a row to 11.25%, signaling a sixth rate cut ahead of its March meeting.

Analysts surveyed by the bank expect it to reach 9% by the end of the year, but there is little room for it to go beyond that given robust inflation expectations.

Brazil will also report year-end industrial production and national unemployment rates for December.

Colombia’s central bank is also almost certain to cut interest rates for the second straight month, but analysts are divided on the size of the cut. Since December’s inflation rate was lower than expected, I persuaded the bank to lower the rate by half a percentage point to 12.5%.

Chile’s central bank has far more room to maneuver and could vote to lower the rate by 100 basis points to 7.25%. Economists surveyed by the bank expect inflation to return to its 3% target this year.

On the inflation front, data from Peru’s metropolitan capital Lima could show consumer price inflation accelerating from 3.24% in December. Brazil reports the country’s most extensive inflation measure, the IGP-M price index, which receives little attention.

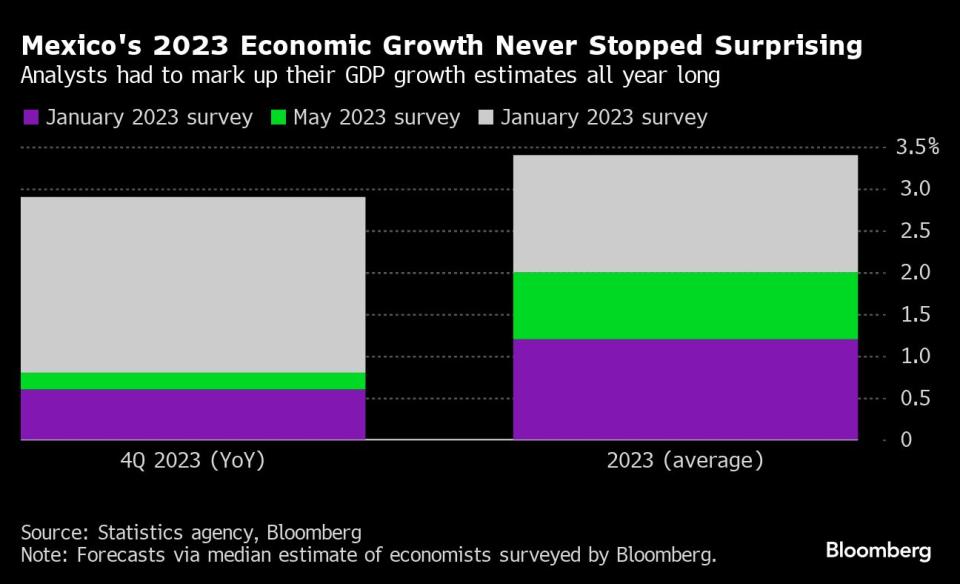

Rounding out the week, Mexico’s fourth-quarter production report is expected to be revised down quarter-over-quarter from the 1.1% pace seen in the three months to September, the lowest in more than a year. This has been slowed by order-of-magnitude borrowing costs.

—With assistance from Robert Jameson, Piotr Skolimovsky, Laura Dillon Cain, Paul Jackson, and Monique Vanek.

Most Read Articles on Bloomberg Businessweek

©2024 Bloomberg LP

[ad_2]

Source link