stocks")

[ad_1]

Soundhound AI has been a big hit on the stock market in 2024, with an impressive 288% gain so far. Investors continue to buy shares in this company based on the belief that this voice artificial intelligence (AI) solutions provider could be the next big thing in AI.

The company’s revenue is growing at an impressive pace, and it also boasts a solid pipeline that will help sustain its breakneck growth in the future.Plus, SoundHound AI stock receives a vote of confidence from his AI pioneer Nvidia (NASDAQ:NVDA)owns a small stake in the company. This is a big reason why SoundHound stock has risen over the past month or so.

But investors looking to buy AI stock now may not feel comfortable paying 42 times Soundhound’s sales. This is much higher than the tech sector average of 7.1x. Of course, it may become a major player in the AI market in the long run, but SoundHound AI is currently very small and far from profitable. Instead, an investor would do well to next buy stocks in two established AI companies that appear to be undervalued.

1. Nvidia

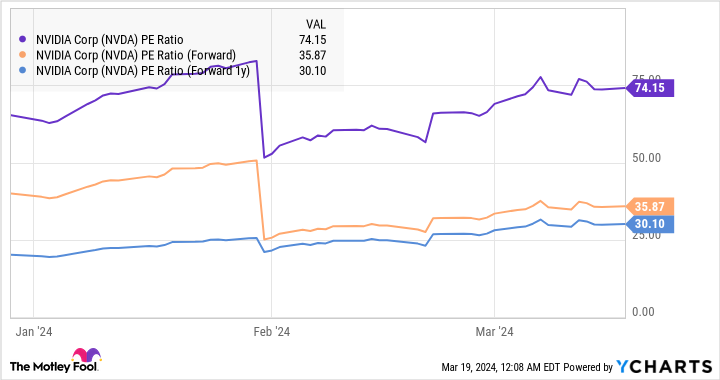

You may be wondering why Nvidia is an undervalued AI stock. The stock trades at 36x, which isn’t that cheap compared to SoundHound. But a closer look at how fast NVIDIA is growing reveals that investors are indeed making quite a profit on the stock right now.

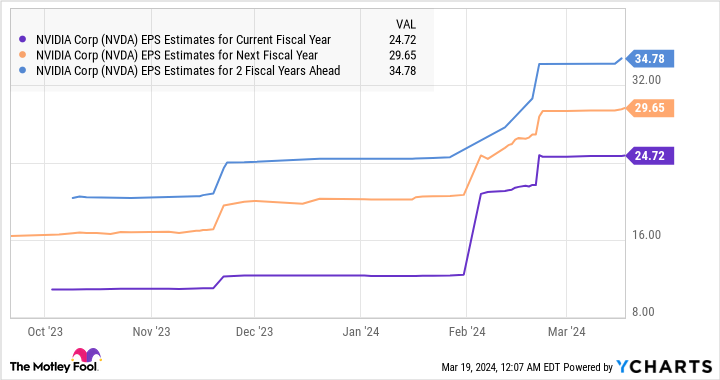

Nvidia’s revenue for the fourth quarter of fiscal 2024 (three months ending January 28, 2024) increased by a whopping 265% year-over-year. Adjusted earnings increased a fast 486% year-over-year to $5.16 per share. For comparison, SoundHound AI’s revenue last quarter was $17.1 million, up 80% year-over-year, and its adjusted loss halved year-over-year to $0.07 per share.

What’s even more impressive about Nvidia is that the chipmaker’s impressive growth will likely continue. The $24 billion revenue outlook for the first quarter of 2025 means NVIDIA’s revenue is on track to once again more than triple his $7.2 billion level in the year-ago period. . Analysts are quickly raising their growth forecasts. They expect Nvidia’s earnings to nearly triple in just three fiscal years, from the $12.96 per share level in fiscal 2024.

This expectation that Nvidia’s revenue will grow rapidly is why the company’s stock trades at an attractive forward earnings multiple. This is evident from the graph below.

Buying Nvidia stock at 30 times fiscal 2027 earnings is a no-brainer right now. That’s because the company trades roughly in line with the 29x forward earnings multiple of the Nasdaq 100 (which uses the index as a proxy for tech stocks). Another clear indicator that Nvidia is undervalued is its price-to-earnings ratio (PEG ratio) of just 0.13. This is a forward-looking valuation metric that helps you understand how cheap a stock is relative to its expected growth.

Traditionally, stocks with a PEG ratio of less than 1 are undervalued. Nvidia’s PEG ratio is well below that mark. All of this indicates that investors should consider buying his Nvidia directly. Nvidia is in a strong position to capitalize on the lucrative long-term growth opportunities that exist in AI chips and deliver healthy returns over the long term.

2. Taiwan Semiconductor Manufacturing

taiwan semiconductor manufacturing (NYSE:TSM)The company, commonly known as TSMC, trades at 10 times sales and 26 times earnings. This means the foundry giant’s stock price is much cheaper than the stock prices of both Nvidia and SoundHound AI.

Given the important role TSMC is playing in enabling the AI chip revolution, investors would do well to get into the stock before the price goes higher. After all, without TSMC’s help, NVIDIA would not have been able to escape the AI semiconductor market. Nvidia is a fabless semiconductor company. In other words, we only design the chips, we don’t manufacture them. His TSMC, Nvidia’s foundry partner, does the actual manufacturing of the AI chips.

It is worth noting that TSMC is the world’s largest foundry company with a large market share of 61%. This far exceeds the 11% share of second place Samsung. The AI chip market is expected to grow at 38% annually through 2030, and TSMC’s dominant position in the foundry space puts it in a good position to take advantage of the growth opportunities on offer.

This is especially true given that the AI chip giant is a TSMC customer.From Nvidia AMD to intel, multiple chip makers are lining up to buy chips made using TSMC’s advanced manufacturing processes. This is why TSMC is focusing on aggressively increasing its monthly manufacturing capacity of AI chips to meet the growing demand from multiple customers.

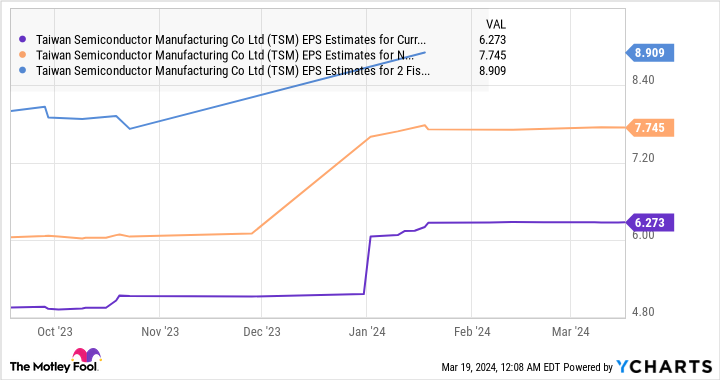

As a result, it would be no surprise if TSMC grows at a faster pace than market expectations from 2024 onwards. Perhaps this is why TSMC’s consensus earnings estimates are trending upwards.

Assuming TSMC reaches $9 in earnings per share in 2026, at which point it trades at a P/E ratio of 29x (matching the forward earnings multiple of the Nasdaq 100 Index), its stock price could jump to $261. There is. This represents a 91% increase from TSMC’s current stock price.

TSMC’s current earnings multiple is lower than the Nasdaq 100 average, meaning investors are currently getting a solid trade on this AI stock. They may not want to miss out on this opportunity, given that the stock price could rise significantly over the next three years.

Should you invest $1,000 in Nvidia right now?

Before buying Nvidia stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks What investors can buy right now…and Nvidia wasn’t among them. These 10 stocks have the potential to generate impressive returns over the next few years.

stock advisor We provide investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks every month.of stock advisor Since 2002, the service has more than tripled S&P 500 returns*.

See 10 stocks

*Stock Advisor returns as of March 21, 2024

Harsh Chauhan has no position in any stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: These are a long call on Intel at $57.50 in January 2023, a long call on Intel at $45 in January 2025, and a short call on Intel at $47 in May 2024. The Motley Fool has a disclosure policy.

Forget SoundHound AI: 2 Undervalued Artificial Intelligence (AI) Stocks was originally published by The Motley Fool.

[ad_2]

Source link