a risky investment?")

[ad_1]

Li Lu, an external fund manager backed by Berkshire Hathaway’s Charlie Munger, says, “The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.” It has even been stated. So when you think about the risk of a particular stock, it might be obvious that you need to consider debt. Because too much debt can sink a company. Points to keep in mind are: Injevity Co., Ltd. (NYSE:NGVT) does have debt on its balance sheet. But is this debt a concern for shareholders?

What risks does debt pose?

Debt and other liabilities become a risk to a company if it cannot easily meet those obligations through free cash flow or by raising capital at an attractive price. Part of capitalism is the process of “creative destruction” in which failing companies are ruthlessly liquidated by bankers. But a more frequent (but still costly) occurrence is when a company must issue stock at a bargain price, permanently diluting shareholders, just to shore up its balance sheet. Of course, many companies use debt to fund growth, and there are no negative consequences. The first thing to do when considering how much debt a company uses is to look at its cash and debt together.

Check out our latest analysis for Ingevity.

How much debt does Ingevity have?

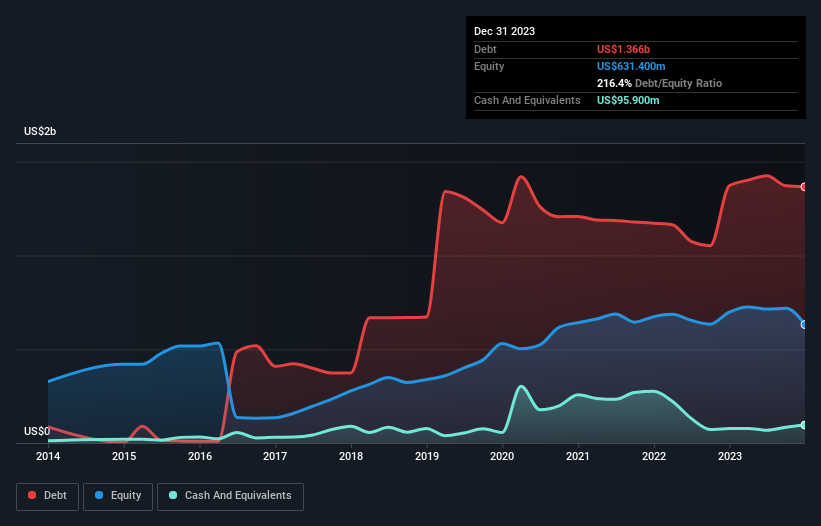

As you can see below, Ingevity had debt of US$1.37b at December 2023, which is about the same as a year ago. Click on the graph to see details. However, she also had US$95.9m in cash, resulting in her net debt of US$1.27b.

How strong is Ingevity’s balance sheet?

The most recent balance sheet shows that Ingevity had liabilities of US$362.9m falling due within a year, and liabilities of US$1.63b falling due beyond that. Offsetting these obligations, the company had cash of US$95.9m on him and receivables valued at US$211.0m due on him within 12 months. So its liabilities outweigh the sum of its cash and (short-term) receivables by US$1.69b.

Given that this shortfall exceeds the company’s market capitalization of US$1.64b, you might want to review the balance sheet carefully. In a scenario where the company has to clean up its balance sheet quickly, we think shareholders are likely to suffer significant dilution.

By looking at net debt divided by earnings before interest, taxes, depreciation, and amortization (EBITDA) and calculating how easily earnings before interest and tax (EBIT) can cover interest, profitability can be calculated. Measures a company’s debt load against. Expenses (interest burden). The advantage of this approach is that it takes into account both the absolute amount of debt (net debt to EBITDA) and the actual interest expense associated with that debt (interest cover ratio).

Ingevity’s debt is 3.4x its EBITDA, and its EBIT covers its interest expense 2.9x. This suggests that debt levels are significant, but not problematic. To make matters worse, Ingevity’s EBIT tank grew by 25% in the last twelve months. If earnings continue at this rate over the long term, the chances of paying off the debt will increase as a result of a snowball effect. The balance sheet is clearly the area to focus on when analyzing debt. But ultimately, Ingevity’s ability to strengthen its balance sheet over the long term will depend on the future profitability of its business. So if you want to see what the experts think, you might find this free report on analyst profit forecasts to be interesting.

But final considerations are also important. This is because companies cannot pay their debts with paper profits. I need cold cash. So it’s clear that we need to check whether that EBIT is leading to corresponding free cash flow. Over the last three years, Ingevity recorded free cash flow equivalent to 50% of her EBIT. This is about normal considering that free cash flow does not include interest and taxes. This cold cash means it can reduce debt if needed.

our view

We’d go so far as to say that Ingevity’s EBIT growth was disappointing. But at least the conversion of EBIT to free cash flow isn’t too bad. We’ve been clear that we think Ingevity is actually quite risky as a result of its balance sheet strength. For this reason, we are quite cautious about this stock and think shareholders should monitor its liquidity closely. When analyzing debt levels, the balance sheet is the obvious place to start. Ultimately, however, any company can contain risks that exist outside the balance sheet. For example, we identified 1 warning sign for Ingevity What you need to know.

If you’re interested in investing in a business that allows you to grow profits without taking on debt, check this out free A list of growing companies that have net cash on their balance sheet.

Valuation is complex, but we help make it simple.

Please check it out Originality and ingenuity Could be overvalued or undervalued, check out our comprehensive analysis. Fair value estimates, risks and caveats, dividends, insider trading, and financial health.

See free analysis

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.

[ad_2]

Source link