[ad_1]

After weathering the coronavirus crash, a once-in-a-generation inflation war and a three-year bear market in Chinese stocks, Asian distributors and their customers are focusing on two key themes.

Luke Brown, head of Asian asset allocation at Manulife Life, said market volatility and a possible China resurgence are top concerns for distributors and investors in Asia.

Mr Brown said Financial Services Agency“For the past 18 months or so, the conversations we’ve had with our distributors and customers have centered on two things: the market is volatile, and when will Chinese stocks recover? .”

Due to the prevalence of these themes in discussions, the company is launching the Manulife Defined Return Fund to address these two concerns of Asian distributors and customers.

“The idea is that there are a lot of customers who remain allocated in cash and obviously they are making a reasonable profit. We’re getting it,” Brown said. (photograph) Said.

“This provides an opportunity to re-enter the market for the possibility of enjoying excess returns without the downside.”

The proposed fund would invest at least 90% of its assets in two-year US Treasuries and up to 10% in derivatives based on the value of the Hang Seng Index.

To build his portfolio, Brown said he will target 0.75% U.S. Treasuries dated March 31, 2026.

This will be purchased together with a digital option designed to earn a bonus coupon of approximately 14% if the Hang Seng Index reaches 108% of the Hang Seng closing price on or around March 12th.

The fund’s IPO period will begin on February 19th and is scheduled to end on March 8th, 2024.

But one of the risks of investing 90% of a fund’s assets in two-year Treasuries is that the value of Treasuries will decline if the Fed raises rates again.

Brown acknowledges this risk, saying: “Obviously, if the two-year rate goes up, the NAV goes down. But that’s just a mark-to-market. After two years, the customer gets 101% back.”

He added: “We don’t foresee any rate hikes. It’s not impossible, but it’s unlikely.”

“What could potentially happen is that the further we get away from easing the financial cycle, the more aggressive the Fed will likely have to be.”

But Brown stressed that the product was not designed with interest rate trends in mind.

“The principle here is a fixed investment period,” he said. “We are taking advantage of today’s rising interest rates and using them to finance our derivatives exposures.”

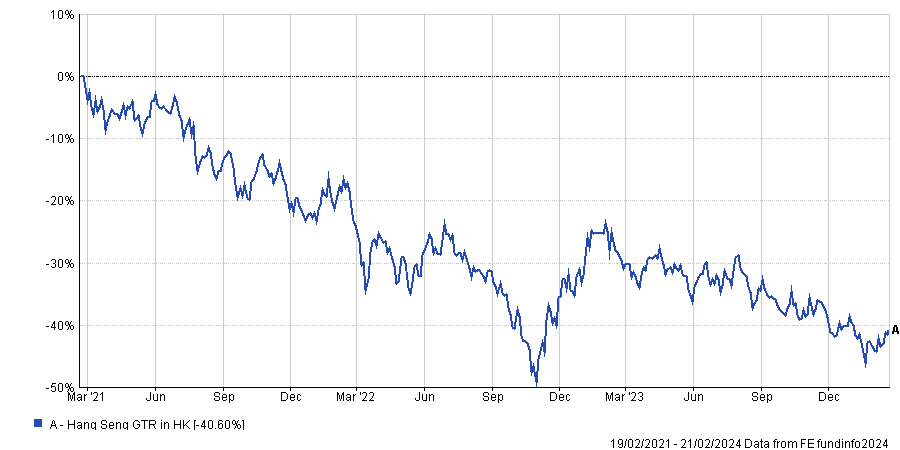

Hansen set for bounce.

The bet on the Hang Seng Index comes as the stock market has fallen for the third consecutive year due to a technology crackdown, repeated coronavirus lockdowns and a prolonged downturn in the real estate market.

The duration and depth of the bear market in Hong Kong-listed stocks has investors starting to wonder whether a recovery in Chinese and Hong Kong stocks will really happen.

“Sentiment is bad. Foreign direct investment in China has collapsed,” Brown said. “But it’s often darkest before dawn.”

“One of the things we consider in our investment decisions is investor sentiment, and sentiment towards Hong Kong stocks and China stocks has been shattered.”

“When we hit that low point, we see a rapid turnaround in sentiment, an influx of capital flows, and a tendency to outperform the market.”

He focused on the valuation of the Hang Seng Index, which has a P/E ratio of 8.8 times as of the end of 2023, compared to the S&P 500 Index’s P/E ratio of about 27 times.

“Of course, we have to be careful that this is not a values trap,” he says. “However, all of this together weighs heavily on the potential recovery of these markets, given that the People’s Bank of China is likely to continue to have an impact on markets as they seek to stabilize and return to a growth trajectory. I think it would be a good story.”

The firm had been underweight Chinese and Hang Seng stocks over the past year, but has since cited an opportunity for “potential near-term tactical upside” in Chinese stocks in its latest Q1 2024 outlook, and has Adjusted the view of allocation.

[ad_2]

Source link