looks attractive based on low valuation and new initiatives")

[ad_1]

PayPal (NASDAQ:PYPL) stock has been sitting in storage for a long time, but the stock looks attractive based on its cheap valuation and new strategic initiatives announced at a first-look event. I’m bullish on this underperforming fintech stock based on management’s renewed growth efforts and its tough assessment.

New Strategy Revealed: Living in the “Fast Lane”

New CEO Alex Criss left Intuit (NASDAQ:INTU), who plans to acquire PayPal in September, spoke of PayPal’s plans to “shock the world.” The company announced that it will unveil its new plans at a “first look” event held yesterday.

Perhaps the plan wasn’t as innovative as some investors and analysts had hoped, as the market seemed overwhelmed by the strategy update as the stock fell 3.7% on the day.

But despite the apparent lack of market enthusiasm in the short term, the new initiatives announced by the company are well positioned to position PayPal for further long-term growth. looks like. Below we discuss some of the most interesting highlights.

PayPal’s new Fastlane initiative looks particularly promising. Finding and entering credit card numbers and remembering usernames and passwords can make the online checkout process a hassle. E-commerce vendors are well aware that any issues or disruptions in the checkout process can significantly reduce conversion rates, and Chris says that online shoppers approximately 50% of the time I stated that I was unable to complete the purchase.

Fastlane aims to significantly reduce this friction and improve the experience. Users can save their information with her Fastlane and “checkout with just her one tap, without giving the member a username or password.” There is no personal information to update. You don’t have to share your credit card with companies on the web. ”

This will be a big problem for both customers and businesses alike. Consumers will enjoy an easier and faster checkout process, while sellers will benefit from higher conversion rates, which should lead to higher sales. Fastlane is currently in a pilot phase, and if it takes off, it looks like it will be a win-win for him, his customers, merchants, and PayPal itself.

If Fastlane is successful, more customers and vendors will be eager to use PayPal. PayPal currently owns the e-commerce platform Big Commerce (NASDAQ:BIGC) say conversion rates can be as high as 70%.

PayPal is also rolling out Smart Receipts. These smart receipts not only allow customers to track their purchases, but also use AI to suggest products the customer might want to buy next, and give each customer personalized cashback offers. can. Emails with PayPal already have high open rates (around 45%, according to Chris), and leveraging this to create personalized offers and recommendations could be a real catalyst for merchants. there is.

Other efforts include the Advance Offers Platform. It aims to personalize how it serves ads online based on customers’ shopping habits, right down to SKU numbers. PayPal says it leverages data from more than $5 trillion in merchant transactions around the world to “customize offers like never before.”

Another initiative, CashPass, gives U.S. customers access to personalized cashback offers from top merchants. Chriss said: “When you see an offer you like, just tap on it. Then, when you shop with that business, this deal is automatically applied when you check out with PayPal. One tap, it’s that easy.” CashPass It will launch in March and include companies such as Uber (New York Stock Exchange: Uber), Walmart (New York Stock Exchange:WMT), McDonald’s (New York Stock Exchange:MCD).

These changes will make PayPal a more integral part of the online shopping process for both consumers and merchants, and should increase PayPal’s stock price in the long run.

PayPal stock is cheap

Unlike other fintech companies that have fallen from their peak, PayPal stock has been profitable. And it’s trading at an undemanding valuation. PayPal’s P/E ratio is just 11x. This is only half of the valuation traded in the broader market. S&P500 (SPX) has an average price-to-earnings ratio of 21.5.

It’s also much lower than the valuations PayPal has typically enjoyed in the past. During the heady days of 2020, PayPal stock traded at more than 100 times earnings. Obviously, this was a little frothy, but as of January last year, PayPal was trading at nearly 40x his earnings, about 4x its current multiple.

I’m not saying that PayPal necessarily deserves a P/E ratio of 40x, but it does show how cheap the stock is compared to its historical valuation, and there is an upside between 10x and 40x P/E. There’s plenty of room.

Is PYPL stock a buy, according to analysts?

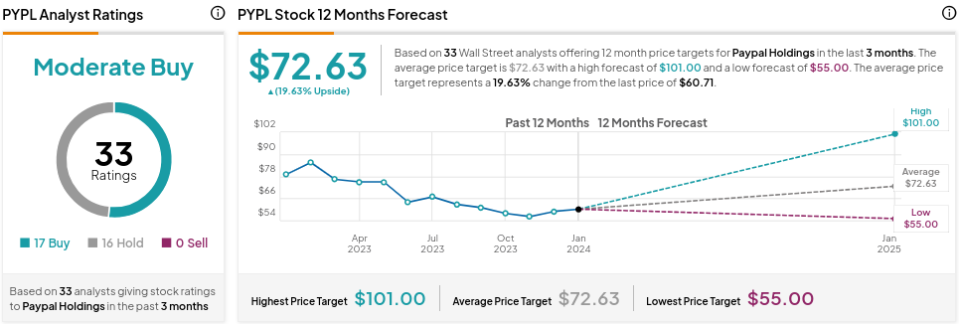

Turning to Wall Street, PayPal received a Moderate Buy consensus rating, based on 17 Buy, 16 Hold, and 0 Sell ratings assigned over the past three months. PYPL’s average price target of $72.63 implies an upside potential of 19.6%.

Lesson: There are signs of life.

PayPal stock has fallen significantly since its glory days. However, the new CEO’s plans have the potential to boost stock prices. The announcement of this plan didn’t cause a stir in the market yesterday, but it should help the stock position itself for longer-term growth. Additionally, the stock’s valuation is less demanding, so it could be a great time to invest. PayPal will report his earnings on February 10th, so there may be some volatility leading up to this report, but his PayPal looks like an interesting buy low for long-term investors.

disclosure

[ad_2]

Source link