[ad_1]

That skepticism, they argued, is rooted in weak emerging markets, a lack of asset sales to prove value, and a lack of transparency regarding investments in individual funds.

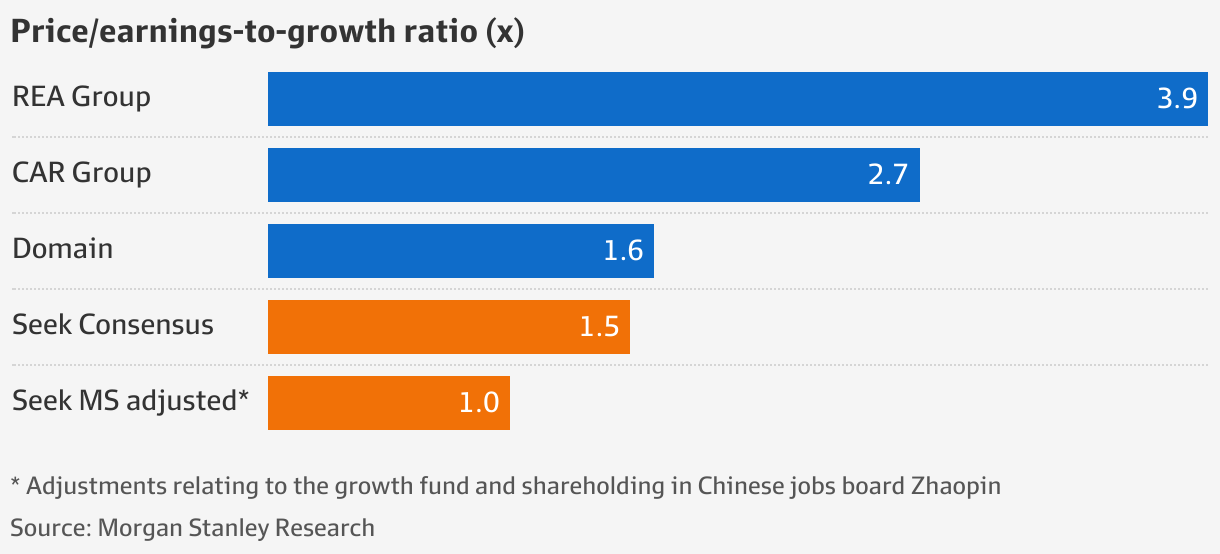

“[Other investors] In fact, some companies go further and apply discounts to core seek multiples due to governance or questionable capital allocation decisions,” McLeod and Bolas wrote in a Feb. 21 note to clients. wrote.

“While the fund’s managers likely have great confidence in the fund’s prospects and given valuations, it is likely that outsiders conducting research without meaningful data could have the same optimism. It’s very difficult to share a different perspective.”

Mr Sheikh declined to comment, while the Growth Fund and Mr Bassat did not respond to requests for comment via Sheikh.

Other shareholders thought Seek was worth $5 a share, or more than a premium, based on the $1.9 billion in cash it received from its VC interests. Seek’s market capitalization was over $9 billion as of Friday’s close, and it trades at a lower multiple than other online advertising companies.

Morgan Stanley presented Sheik with several options for improving the way investors value funds and argued that ratings should not be lowered from current levels. Seek may sell all or part of its 84% stake, the Fund may sell some assets to prove its value, or Seek may redeem its shares for cash in 2026 under the terms of the agreement. there is a possibility.

McLeod and Boulas, who are bullish on Seek, added that external factors, such as a turnaround in technology companies and more positive sentiment, could also lead to change. They argue that one should not discount the apparent value of a fund as reflected in seek stocks.

Seek’s ownership interest is valued at $1.9 billion, and the company pays approximately $20 million in annual management fees that are recognized as an expense in the income statement. Seek’s net debt was $1.1 billion as of Dec. 31.

[ad_2]

Source link